Q1 2020 Report – Macro perspectives on Spain - BFF Banking Group

Report on Macro perspectives on Spain

and its regional governments’ finances

Q1 2020: COPING IN THE ERA OF COVID-19

Executive Summary

Looking beyond uncertainty

Once the first quarter of 2020 came to an end, it had already become clear that "COVID-19" would become the buzzword of the year. The initial macro recovery expected for 2020-2021 had derailed due to a “once-in-very-hundred-years” event with a global impact. For this reason, the situation remains fluid and it is yet too early to come up with reasonable quantitative estimates on its impact, even tough as time goes by we have greater knowledge of the impact that the confinement measures adopted worldwide are having on GDP growth and on public deficits. In both cases, the level of deterioration of these two indicators is expected to go even beyond those registered during the last global crises, the financial crisis of 2008-2009 and the 2011-2012 sovereign debt crisis in the eurozone.

Initial estimates before the Covid-19 outbreak reported a scenario in which the economic slowdown could bottom out in 2020 to 1.6%, while, on the other hand, the expected bounce back of the international economic environment would have pushed for a moderate economic acceleration which, in turn, would have allowed economic growth levels to reach closer to 1.9%. This increase in economic dynamics would have supported the creation of more than 600,000 jobs in 2020 and 2021 (34% less than those created in previous years) and would have reduced the unemployment rate to an average of around 12,5% in 2021. These estimates were coherent with the expected global growth of 3.2% in 2020 and the gradual economic acceleration that would have translated into a global economic growth of 3.3% in 2021.

Even though it is yet too early to have a full grasp and clear estimates on the level of impact of the coronavirus on the figures of GDP growth, and provided also that Spain is the European economy most reliant on tourism within the EU, with a relative share of 12% of the Spanish GDP stemming from revenues of this sector , it can be estimated that GDP growth in Spain in 2020 could in all reality be closer to an interannual drop of -8%, while the economic rebound in 2021 could stand around 5%, according to the latest macro estimates by IMF. Thus, Spain would be one of the countries in the eurozone suffering the most severe economic impacts due to the pandemics, only surpassed by Italy in this regard.

Spanish GDP can contract by up to 13,6%

In its most recent projections for the Spanish economy, the Bank of Spain estimates that in case the state of alarm prolongs itself for a total of eight weeks (until mid-May), the Spanish GDP in 2020 would shrink between 6,6 % and 8,7 %, depending on the level of persistence of the impacts to be registered well beyond the end of the confinement (in particular, in the sectors most exposed to touristic activity), which could in turn lead to new potential outbreaks of the epidemics. In a scenario that would combine a state of alarm of a total of twelve weeks along with a greater persistence of the effects well beyond the confinement has ended, for which the affected sectors would not return to a level of production equivalent to the one they held at the end of 2019 until the last trimester of 2020, the Bank of Spain estimates that GDP in 2020 could fall by 13.6%.

Increase in public deficit is reason for concern as procurement costs of the crisis run high

In all instances, the different scenarios devised show that the budgetary costs of the recessive episode caused by Covid-19 will be extremely high, because of both the measures adopted and, most importantly, the performance of the automatic stabilizers. According to the different scenarios considered, the public deficit could stand between -7% and -11% of GDP in 2020. With regards to public debt, it would be expected to stand approximately between 110% and over 120% of GDP, which is a record figure in modern times.

Transport and tourism are the most vulnerable sectors

Most recent evidence on the economic activity show a significant worsening of the economic environment in all geographical areas, particularly in the countries with the most severe outbreaks of the virus and that have, therefore, been forced to adopt drastic measures to contain the epidemics. For similar reasons, the decrease in the economic activity is most pronounced in sectors such as tourism and transport.

In the last decade, a tightening of financial conditions for fears of recession have often been met with a more accommodating monetary policy, which has driven up recovery. This same strategy is being employed during this epidemic, with an unprecedented level of stimulus to the economy being adopted, both through monetary policy, with the FED and the ECB stepping up the pace and increasing the size of their balances at an unprecedented rhythm; and via the fiscal stimulus provided by the governments of the most developed economies. In the short run, and over the last weeks, the result of this combination of monetary policy and fiscal stimulus has significantly mitigated the impacts on debt markets.

Covid-19 crisis is different from any others: a combined shock to supply and demand

However, the reasons why all could be different in this crisis should also be highlighted: the pandemics originated by a Coronavirus introduces a combined shock to both supply and demand. Up until now, previous recession periods that we’ve witnessed since 2008 have been mostly characterized by shocks to the demand side, which the monetary policy instruments are well-equipped to address. However, since the current situation also affects supply, this could well translate into actual shortage of goods, which in turn could render this crisis an inflationary one as well, even though it is yet to early to anticipate such scenario.

Recovery in the services sector will be more slow-paced

The most relevant economic impact stemming from the current health emergency affects the services sector, which accounts for approximately 75% of the GDP of developed economies.

In the manufacturing front, as things return to normal and the confinement measures start being lifted, there’s an inherent “pick-up” of activity: companies increase production and rebuild their stocks, which allows this sector to recover with relative haste in the short term. However, in the Services sector this is not so much the case – these services compose the largest proportion of the global economy and GDP lost in that front is rarely recoverable. It should also be expected that the restraining and confinement habits recommended to citizens in order to avoid contagion will continue well beyond the fear of contagion has died down, which will extend the economic effects of the sanitary crisis in time.

The reaction of an economy at an already weak starting point

In addition, at a global level the economies were already at a very weak starting point when the crisis emerged. Japan was on the brink of recession before the impact of COVID-19 reached them; China reached an all-time-low in its annual growth figures last year, the worst registered in the last 30 years; Germany was also on the brink of a technical recession over the last trimesters of 2019 and our initial growth estimates for the eurozone in 2020 were already revealing a growth below 1% in this area.

Regions fiscal position to worsen again in 2020

Regarding the Spanish public administrations, the political situation has negatively impacted the fiscal positions of the Spanish regions. In this regard, the fiscal deficit of the Spanish regions in 2019 (-0.55% or -0.35% if we deduce the effects of the 2017 VAT settlement) was significantly higher than in 2018 (-0.28%), despite the improvement registered over the last months of 2019 due to the disbursement of current State transfers to the regions; in this second scenario, only six autonomous communities (CCAAs) have reached the deficit target of -0.1% in 2019.

The last meeting of the Council on Fiscal and Financial Policy that took place January last between the Minister of Finance and the Communities (CCAAs) – and the first celebrated since 2018 – resulted in the revision of the debt and deficit targets of the regions for the upcoming years. Thus, the regional deficit target was revised to 0.2% of GDP for 2020, instead of the initial 0.0% foreseen. With regards to the deficit targets for 2021-2023, the regional deficit was set at 0.1% of GDP and at a budgetary equilibrium (0.00%) for 2022 and 2023. As a result, the objective of reaching budgetary equilibrium has been delayed for two years until 2022. Naturally, the deficit targets could likely suffer further revision in order to accommodate the current reality of the Spanish public accounts as a result of the Covid-19 pandemics.

Prior to the outbreak of COVID-19, it was expected that 2020 would again show for an improvement in the deficit figures of the regions. The independent tax authority (AIReF) considered that, in aggregate terms, it would be “tight, but feasible (43% probability)” that the regions would meet the 2020 initial deficit target of budgetary equilibrium (budgetary equilibrium was defined in 2017 and it was based on this objective that the Communities (CCAAs) planned their budgets for 2020).

Moody's was the first rating agency to provide new projections on the expected deterioration of the regional deficit figures in 2020 due to the additional expenditure incurred in face of the COVID-19 outbreak. In this regard, the agency expects the regional deficits in 2020 to oscillate between 1.7% and 2.8%, in levels equivalent to those registered in 2012-2013.

Regional financial debt could increase by 12% in 2020

The financial debt/GDP ratio of the regions had been stabilizing over the past years, even though these were still at much higher levels than those registered prior to 2007. Nevertheless, and to the resemblance of the regional deficits, Moody’s anticipates an increase in the aggregate regional debt of approximately 12% to reach on average EUR 330bn by the end of 2021, in comparison with the EUR 295bn of the regional financial debt at the end of 2019 (approximately EUR 304bn at the end of 2020). At the end of the Q3 2019, the financing instruments of the central government represented 60% of the total balance of the regional debt. The Spanish regions increased the levels of their aggregate financial debt to EUR 298bn at the end of September 2019, which still shows for q/q decrease of EUR 2.55bn and an interannual decrease of EUR 5.63bn, which represents 24.1% of the Spanish GDP. The communities of Catalonia and Valencia alone represented a combined value of EUR 127bn of financial debt, which account for 42% of the total regional financial debt.

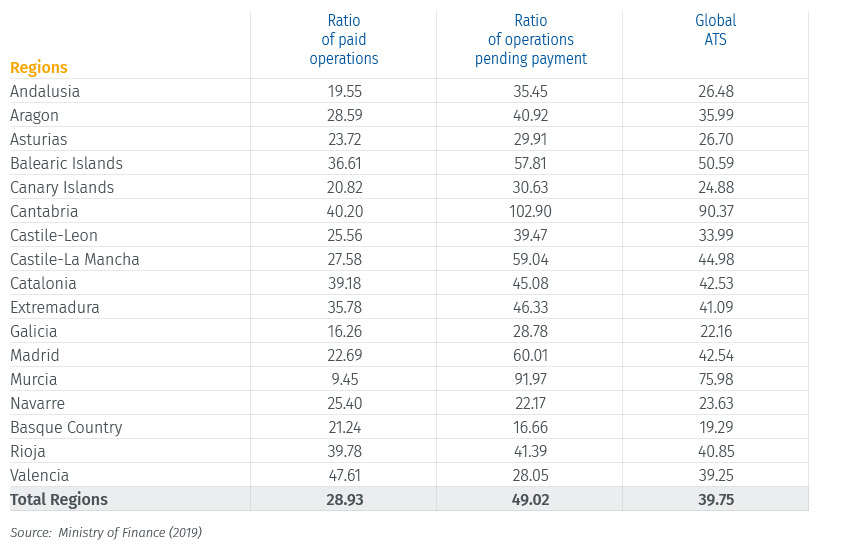

The latest figures on the average payment time at November 2019 show an average time for payment to suppliers (payment days start to accumulate as soon as the invoice has been registered or the work certificate approved, as per the new methodology defined in royal decree 1040/2017) of 39.75 among the autonomous communities, which stands 9.75 days above the 30-day timeframe foreseen by law. Both Valencia (since June 2016) and Murcia (since February 2017) remain under strict control, in line with the provisions of Article 25 of the LOEPSF (Organic Law on Budgetary Stability and Financial Sustainability), since both regions have failed to meet the 30-day limit for six consecutive months. In January 2020, the Spanish government decided to apply to Murcia the coercive protocol as described in Article 26 of the LOEPSF (Organic Law on Budgetary Stability and Financial Sustainability). In spite of the larger transfer amounts that the autonomous communities will receive and the fact that these will be done at an earlier stage in order to avoid liquidity tensions during this period, we still expect to see a progressive increase in the Payment times (PMPs, plazo medio de pago) in 2020, as the deficit of the communities increases due to the additional health spending needed to face the pandemics.

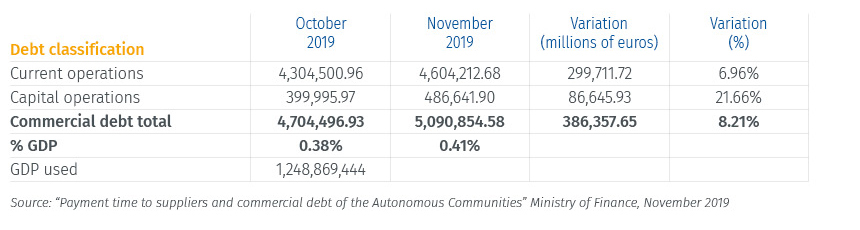

Concerning the evolution of the commercial debt of the regions, at the end of November 2019, the commercial debt (non-financial) of the Autonomous Communities, defined as the payment-pending transactions as per the Royal Decree 635/2014 of July 25, rose to EUR 5.090,85mn, which represents 0,41% of the Spanish GDP. 90,44% of commercial debt is concentrated in current operations with an amount of EUR 4.604,21mn, while the remaining 9,56% equal to EUR 486,64mn and are stem from capital operations.

FIGURE 1 | Spanish regions’ average payment periods as of November 2019 (days)

FIGURE 2 | Total Commercial debt of Autonomous Communities

Local entities will not be as affected by deficits as the communities

With regards to local entities, the initial scenario prior to COVID-19 considered that, on aggregate terms, the local surplus could have been reached in 2020, at around 0,4% of GDP, thus maintaining the expected figure for 2019. The original estimates for 2019 and 2020 showed a slight attenuation in the reduction of local debt, which is consistent with the expected decrease in the budgetary surplus. The latest quarterly data on local debt published by the Bank of Spain and concerning the third trimester of 2019, revealed a reduction of less than EUR 500mn, which stands way below the decrease registered for the same period in 2018 of almost EUR 1.100mn.

By the end of 2020, AIReF does expect the aggregate financial debt of local entities to stand around at 1.5% of GDP (before COVID-19), thus comfortably meeting the 2.0% target. The last published annual statistics of the Bank of Spain of 2018 show a debt/GDP ratio of 2.1%, way below the short-term target of 3%. Naturally, these figures would need to be placed into perspective and subject to revision due to the pandemics, but municipalities will surely be less impacted than the communities (CCAAs), as the latter are responsible for most health expenditures.

Moreover, the municipalities may use the surplus accumulated over the past two years in the employment of measures directed at the mitigation of the pandemics.

The largest municipalities have done an important effort to reduce their indebtedness since the entry into force of the LOEPSF (Organic Law on Budgetary Stability and Financial Sustainability) in 2012 and up until 2018 and, on average terms, the financial debt/current income ratio has been reduced from an average of 100% of current income to 47% at the end of 2018.

At first, the trend was expected to continue in 2020 and 2021, with an average debt/current income ratio of the largest grouping of municipalities at around 40% in 2020.

Though an improvement in expenditure in 2020 is not expected due to the costs of COVID-19, the financial positions of the municipalities will, in any case, continue to be significantly more solid on aggregate terms in 2020 than those of the communities (CCAAs).

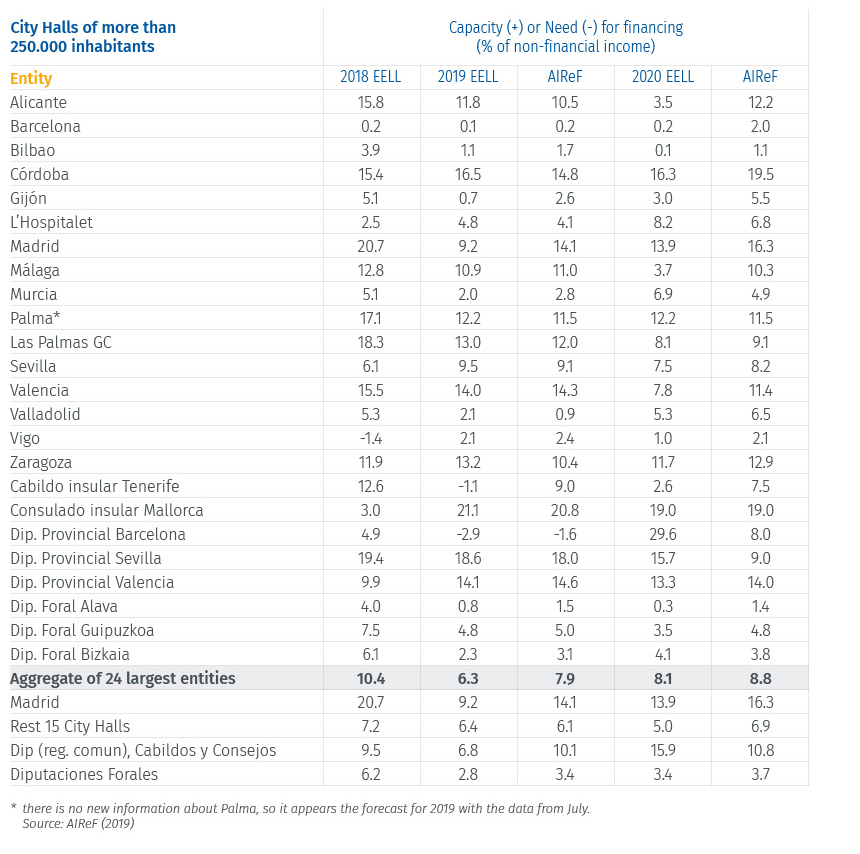

FIGURE 3 | Capacity/Financing needs in 2018, 2019 and 2020 of the 24 largest local entities. Estimates by local entities and AIREF

Request the full report by sending an email to [email protected]