Report Macro Perspectives Spain 1Q2021 - BFF Banking Group

Macro perspectives on Spain and its regional governments' finances

1Q 2021

Spanish regions and municipalities: growth momentum to accelerate in 2H 2021 but downside risks need to be considered

Executive Summary

The Spanish economy at the start of 2021

According to provisional figures, the Spanish GDP declined by 11% in 2020, an unprecedented record showing the severity of COVID-19's impact on the economy. In the last quarter of 2020 there was a QoQ growth of 0.4%, a figure better than anticipated and better than other eurozone countries, possibly because the severity of the measures applied to contain the advance of the virus was lower in Spain than in other countries, but insufficient to move at a desirable pace in the recovery of the lost GDP. It also reflects a severe slowdown from the QoQ growth of 16.4% in the third quarter of 2020, the highest increase in real terms of the historical series, as a result of the growth in domestic demand because of the easing of restrictions on mobility and the reduction of uncertainty regarding the pandemic, as well as a more positive than expected evolution in household income and wealth.

In 2020, the only sectors that recorded growth in their GVA were the primary one and services of the public administrations. Excluding these, the fall in GVA in non-agricultural market services was 14%. Within this group, the impact of the crisis was very uneven. Thus, while in the activities most affected by the crisis – trade, transport and hospitality, together with artistic and recreational activities – the fall of the GVA was 24%, in the other sectors – without agriculture or public administrations– the decrease was 8.5%. This implies that 70% of the GDP lost in 2020 came from the former group of activities.

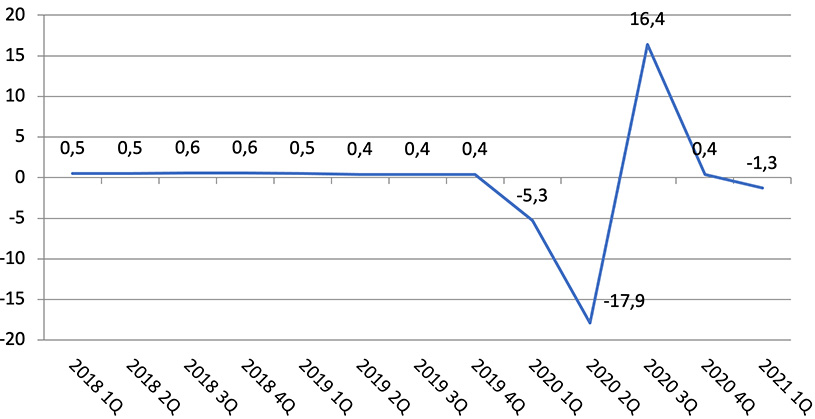

The recovery at the beginning of 2021 is slower than previously expected, as can be seen in Figure 1 showing AIReF's updated economic activity indicator at the beginning of March 2021, which would reflect a decline in GDP of 1.3% quarter-on-quarter, as per available data at early March.

In January, the AIReF real-time indicator still anticipated a positive start to the year, with a GDP increase higher than one percentage point. However, the institution already estimated a 0.8% decline in early February, which has been getting worse at the rate of the weaker macro and employment figures that have been released (see Figure 1).

Figure 1 Decline of economic activity in 1Q21 (evolution of GDP in quaterly rate %)

Source: National Statistics Institute and AIReF

The slow vaccination process, which makes it materially impossible to achieve herd immunity before summer - putting the tourism campaign at serious risk as well as the progressive deterioration in the labour market, cast some shadow on the strength of economic recovery in the second half of the year.

The fact that 98% of the productive fabric in Spain is made up of SMEs or micro-SMEs is one of the reasons why Spanish GDP fell much more strongly last year than its European partners. In this sense, the Bank of Spain warns that "the size of the company remains one of the key factors to explain the recent evolution of both turnover and employment", which is reflected in the fact that the smallest companies are those that declare a worse evolution perceived in this quarter and also less favorable expectations for the second quarter of the year.

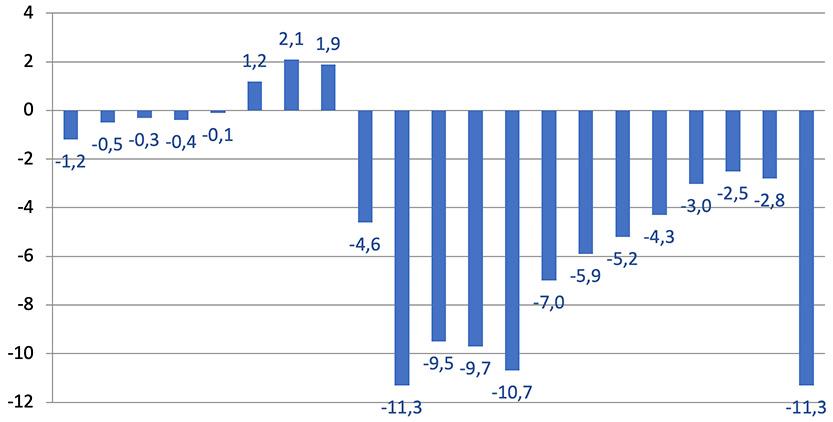

The public deficit could have closed by 2020 at around 11.5% of GDP (Figure 2), a somewhat better figure than the expected one a few months ago; the official figures will be published at the end of March, but the provisional closing figures for the Social Security in 2020, the only ones published at the date of this report, would show a deficit of EUR20bn by 2020 (1.8% of GDP), the highest recorded in the historical series and although State transfers doubled in 2020 vs 2019 (EUE30.3bn vs EU15.6bn), as the aggregate expenditure increased by 9% year-on-year, the biggest increase in the last two decades (see Figure 2).

Figure 2 Evolution of the budget balance in Spain (superavit or deficit % GDP 2000-2020)

Source: Bank of Spain and Ministry of Finance

In any case, and based on historical precedents, closing a double-digit imbalance between revenues and expenditure can take a decade: as an example, the deficit of 11.28% of GDP in 2009 only fell below the 3% threshold in 2018, after undergoing a major fiscal adjustment. Starting from a public debt/GDP ratio of 117% at the end of 2020 and assuming a reduction in the structural deficit of 0.5 per year, AIReF estimates that recovering the public debt threshold endorsed by the EU of 60% of GDP could be delayed until 2050.

The Macroeconomic picture in 2021-2022

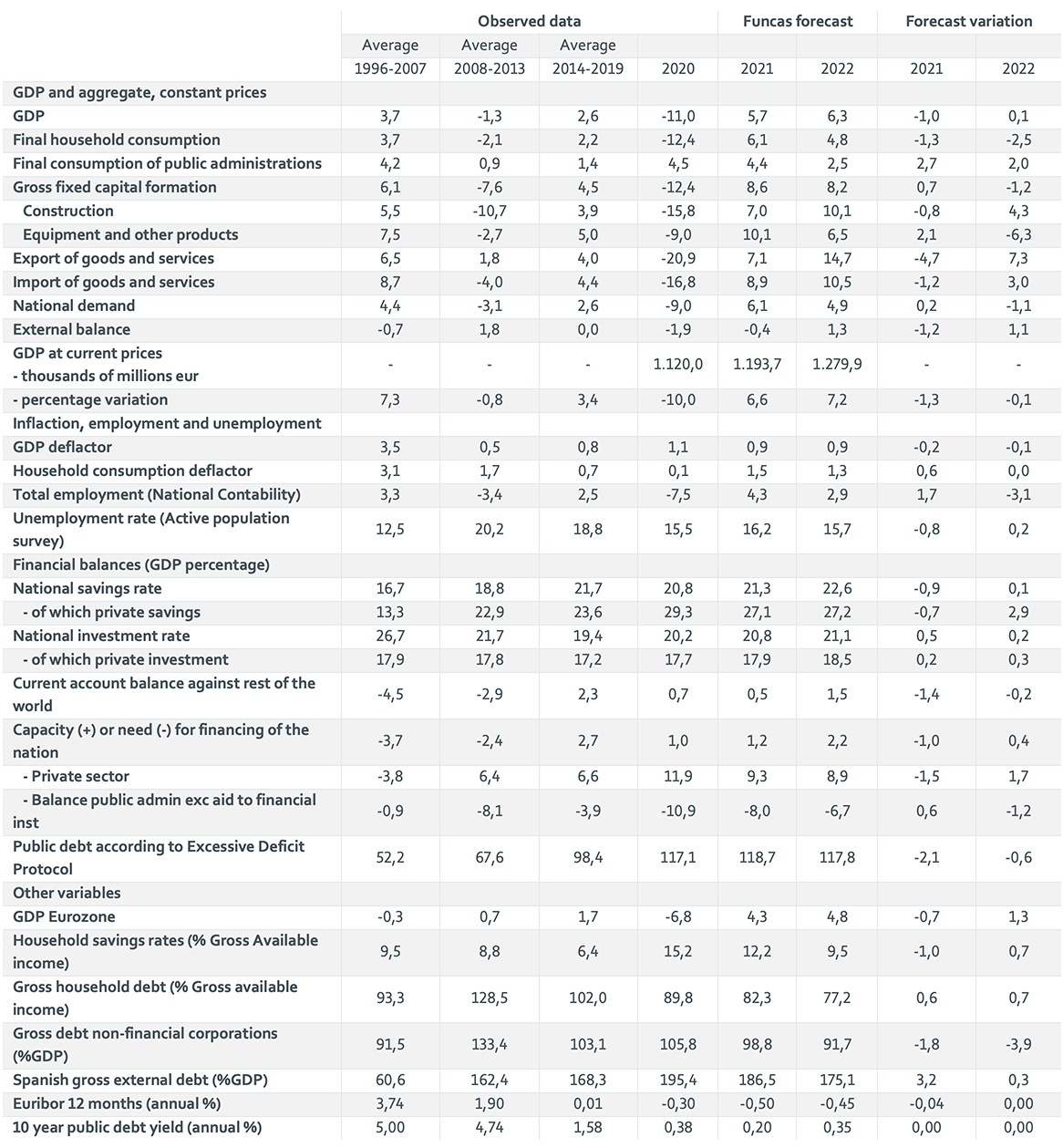

The ongoing dynamics suggest that the recovery path of the Spanish economy will be delayed at least until the arrival of summer, which is why the consensus of analysts have lowered the growth forecast for the Spanish economy in 2021 to around 5.5%, a long way off from the Government's forecasts included in the General State Budget for 2021, which pencils in a GDP growth of 9.8% for this year (or 7.2% if the additional boost from the European funds is not included). The forecasts of the main international organizations are also more in line with a GDP growth scenario in 2021 below the 6% threshold, such as the IMF (5.9%) or the European Commission (5.6%) (see Figure 3).

Figure 3 Spanish economic forecast 2021-2022 (annual variation rates in percentage unless otherwise indicated)

Source: Funcas

The maintenance of strong restrictions on activity and mobility due to the deterioration of the health indicators in the first months of 2021, which led to the implementation of social distancing measures and restrictions on the opening of some businesses, together with the slow progress of the vaccination campaign, weighs down private consumption and keeps the tourism and hospitality sectors at a minimum of activity. Thus, and also considering weakness of domestic demand, we need to consider in addition the contraction in some of the main export markets of the Spanish economy, particularly in Europe, where short-term economic indicators are on decline, especially in Germany and France.

Services, such as hospitality, tourism and retail trade, continue to be the most affected by the restrictions imposed and they show declines in activity similar to those registered during the month of May 2020. This has led to an increase in the use of income protection schemes, such as the Temporary Employment Regulation (furlough/ERTE) and the benefits for self-employed worker in the affected sectors, which has prevented a further deterioration in the labor market.

During the second part of the year there will be a change in the macro trend, as vaccination positively affects the health situation and restrictions are relaxed, facilitating the recovery of private spending and tourism. Our forecasts for private consumption for 2021 (+ 6.1%) and 2022 (+ 6.5%) reflect these factors.

The expansionary momentum from the second part of 2021 will carry over to 2022. As a result, we expect an acceleration in GDP growth to slightly below 7%. The main factors underpinning the economic recovery will operate at full capacity: private consumption will strongly grow thanks to the absorption of a large part of the excess savings generated by the crisis; tourism will gradually normalize, with a summer season that could be closer to pre-pandemic levels; and the stimuli from the European recovery plan could exceed those expected for this year, once the start-up procedures are well established.

The funds associated with the Next Generation EU (NGEU) program will have a growing effect over time, particularly on investment, although there is a bureaucratic procedure, both at the European level and in Spain, which will mean that some projects cannot be started in the first half of the year. Estimates of the impact of these funds on the Spanish economy continue to point to a significant effect this year and the next two years: 1.5 pp of GDP on average per year.

The public deficit will remain at high levels: we estimate 8% of GDP in 2021 and 6.7% in 2022, which will mean an increase in public debt of around 190,000 million euros in the period as a whole, although the debt to GDP ratio will remain at around 118% due to the increase in the nominal GDP. In this scenario, the evolution of foreign tourism will be positive and will present high growth rates, although from low activity levels and with high uncertainty about the persistence of the effect that the pandemic may have on the willingness of people to travel, on the reduction of supply in some market segments and the rising cost of air transport.

With regard to the inflation rate, an increase is expected this year to an annual average of 1.5%, as a result of the increase in the price of oil as well as the recovery of prices in some services that last year registered strong decreases as a result of the crisis, such as hotels, air transport or tourist packages. On the other hand and regarding 2022, a slight decrease in the inflation rate is expected. However, there is a risk of an upward deviation, due to the possibility of a faster recovery in demand than in supply in sectors that are experiencing greater destruction of the productive fabric, such as tourism and restaurants.

Main risks to our macroeconomic scenario 2021-2022

The compliance with the forecasts of the previous sections depends on avoiding the downside risks linked to the management of the pandemic, the solvency of some companies, the effectiveness of economic policy and the adoption of reforms.

In the first place, the speed of the deployment of vaccination and its effectiveness are decisive factors for the summer season. Despite the fact that the population vaccination process has started, there is uncertainty about when the level of herd immunity will be reached and if it will last over time. In addition, we must add the possibility that different regions of Europe and Spain are advancing at different speeds in the immunization process, which would lead to an uneven recovery.

Secondly, the intensity of the recovery will be proportional to the effectiveness of the measures to support companies that have fallen on hard times, despite being viable.

Going forward, it will be necessary to focus on processes that allow the identification of debt that is sustainable, as well as facilitating debt restructuring mechanisms, streamlining out-of-court processes to resolve these types of problems, or encouraging the entry of private capital. In this way, economic policy should not sustain indefinitely a sector that is structurally going to reduce its level of activity, but rather facilitate its adaptation to the new reality and the efficient reallocation of resources.

As in any economic recovery, market expectations play a crucial role. And the latter in turn depend on the ability to implement new reforms, avoiding setbacks in those already adopted and adapting the design of the measures to the objectives of the digital, environmental and social transformation.

A protracted crisis could also leave deep scars on the fabric of the European economy and society, through widespread bankruptcies and higher unemployment as policy support measures are lifted. In turn, bad debts would lead to an increase in non-performing loans, which would cause tensions in the banking sector and financial markets.

Faced with these challenges, special attention should be paid to the evolution of tourism. The sector is about to enter its second year of crisis, with many companies on the brink of insolvency. In our forecasts, the hypothesis of a gradual recovery from the second quarter is assumed, so that the tourism income obtained during the next summer season would be close to the last year revenues, which would be roughly a quarter of the pre-crisis level. The recovery would take hold during the rest of the forecast period. As a result, at the end of 2022, tourism would have recovered 75% of the revenues lost by the crisis.

Finally, the increase in the oil price to 70 dollars per barrel - 78% more than just four months ago, a very significant figure that has not been seen for over a year, and that is well above the forecasts of the Government in the 2021 State Budget (46.6 dollars per barrel) -, would suppose an extra cost of about EUR 8,000mn for the Spanish economy.

Autonomous Communities: extraordinary financing mechanisms and APT

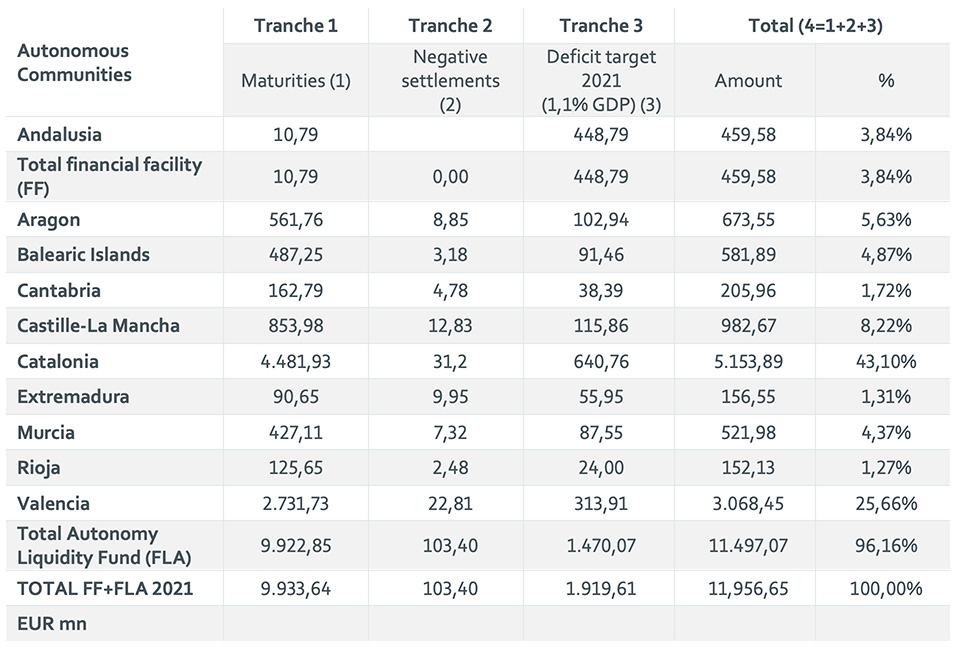

The latest relevant data on the financing of the Autonomous Communities is the breakdown of the extraordinary financing mechanisms by autonomous community corresponding to the first quarter of 2021. In this token, EUR11,965mn granted to the Financing Fund for Autonomous Communities (FFCA) will be distributed in the first quarter of the year among the regions adhered to the Financing Fund (see Figure 4).

Figure 4 Disbursement by regions of the extraordinary liquidity mechamisms in 1Q21 (EURmn)

Source: National Statistics Institute

The estimated initial needs of the Financial Facility and FLA compartments for the entire 2021 financial year amount to 33,909 million euros. Likewise, it is foreseeable that additional resources will be necessary to those provided for in this agreement to finance the 2020 deficit deviations that may occur.

Regarding the average payment time (PMP) of the autonomous communities, this indicator fell for the first time from the threshold of 30 days (26.96 days) since the beginning of the series, in April 2018, with the latest data available until December because of the largest transfers from the State. This month, no community presents an APT greater than the 60-days threshold, the limit from which the Ministry of Finance begins to apply the measures provided for in the stability regulations (see Figure 5).

Figure 5 Average payment period by autonomous communities (days)

Source: Finance Ministry

Regarding the commercial debt, the latest reported figure is EUR 4.38 bn, equivalent to 0.39% of the national GDP. This represents a decrease of EUR 713.88 mn compared to the previous month.

As was the case in previous months, the evolution of the APT and the commercial debt is related to the increase in the processing of operations of a commercial nature, especially in the health sector, as a result of the COVID-19 pandemic. Commercial operations of a healthcare nature originated between March and November have increased with respect to the same period of 2019 by 17.09%.

In this way, the payments made in the last ten months have amounted to EUR 44,165 mn (EUR 35,352 mn in the health sector), which represents an increase of 15.54% (23.42% in the health area) with respect to the same period of the previous year.

Request the full report by sending an email to [email protected]